:max_bytes(150000):strip_icc():format(webp)/inelastic-demand-definition-formula-curve-examples-3305935-final-5bc4c3c14cedfd00262ef588.png)

Elastic and inelastic examples are fundamental concepts in economics that describe how the demand for goods and services responds to changes in price. In this article, we will explore the definitions of elastic and inelastic demand, provide various examples to illustrate these concepts, and discuss their implications on businesses and consumers. Understanding these principles will not only enhance your economic knowledge but also help you make informed decisions in your daily life.

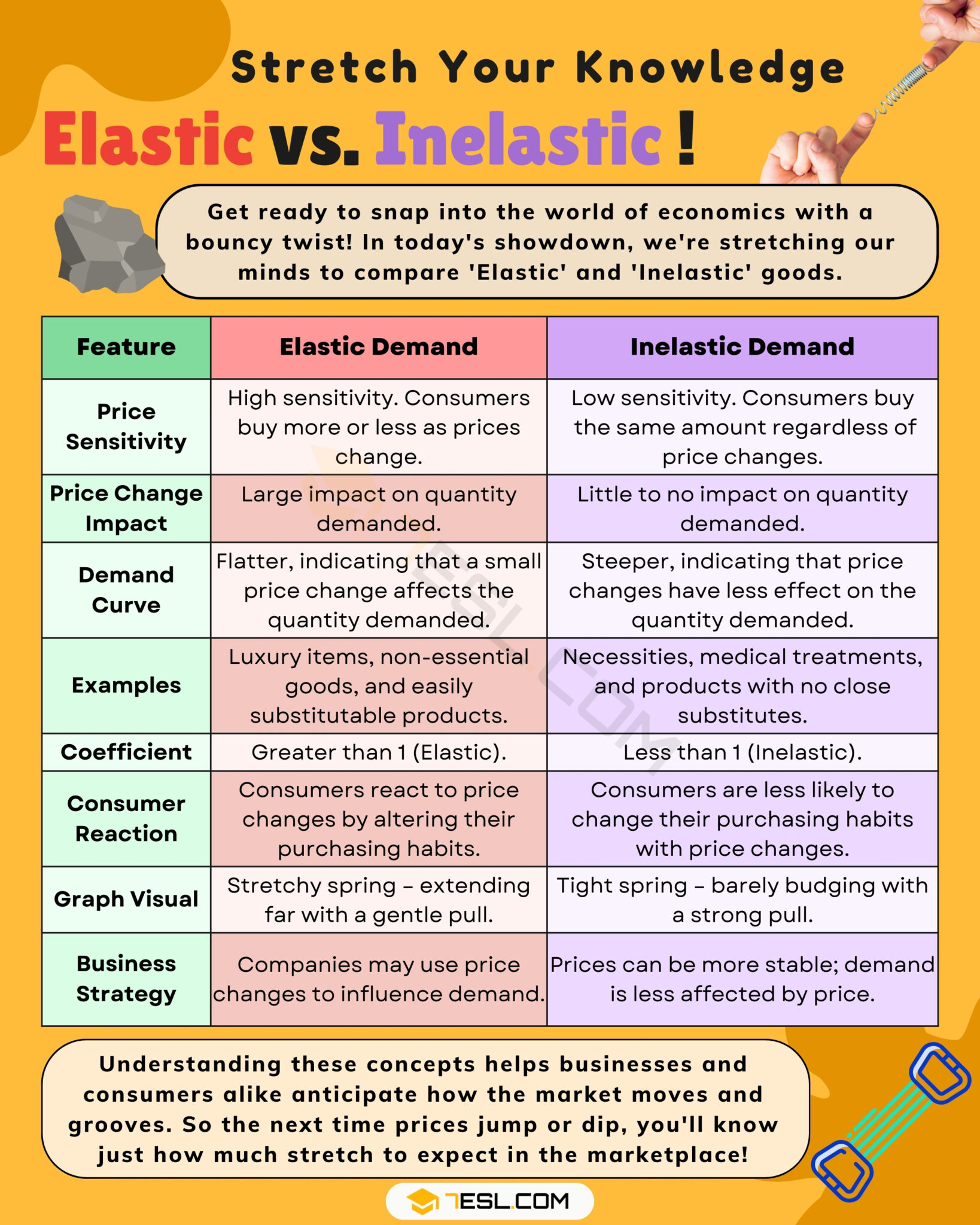

Elasticity of demand is a measurement of how much the quantity demanded of a good changes in response to a change in price. If a small change in price leads to a significant change in the quantity demanded, the demand is considered elastic. Conversely, if a change in price has little effect on the quantity demanded, the demand is inelastic. This article will delve into the characteristics, factors influencing elasticity, and practical examples of both elastic and inelastic demand.

Additionally, we will discuss real-world applications of these concepts, such as pricing strategies for businesses and consumer behavior. By the end of this article, you will have a clear understanding of elastic and inelastic demand, allowing you to navigate economic discussions with confidence.

Elastic demand refers to a situation where the quantity demanded of a good or service changes significantly in response to price changes. The price elasticity of demand (PED) is calculated as the percentage change in quantity demanded divided by the percentage change in price. If the absolute value of PED is greater than 1, the demand is elastic.

On the other hand, inelastic demand occurs when the quantity demanded changes little with price changes. In this case, the absolute value of PED is less than 1. Inelastic goods typically include necessities, where consumers will continue to purchase despite price increases.

Several factors can influence whether demand for a product is elastic or inelastic:

Here are some typical examples of elastic demand:

A study published by the National Bureau of Economic Research found that for luxury goods, a 10% increase in price can lead to a 25% decrease in quantity demanded, illustrating high elasticity.

In contrast, here are examples of inelastic demand:

According to the U.S. Energy Information Administration, a 10% increase in gasoline prices results in only about a 2% decrease in quantity demanded, indicating its inelastic nature.

Understanding elasticity is crucial for businesses when setting prices:

Consumers can benefit from understanding elasticity as well:

Several misconceptions surround the concepts of elasticity:

In conclusion, understanding elastic and inelastic demand is essential for both consumers and businesses. By recognizing how price changes affect buying behavior, individuals can make informed decisions while companies can optimize pricing strategies for maximum revenue. We encourage you to explore more about elasticity in economic discussions and apply these concepts in your everyday life.

Feel free to leave your comments or questions below, share this article with others, or check out our other resources on economic principles!

Thank you for reading, and we look forward to seeing you again soon!